Published: 5 Oct, 2020 CET.Updated: Fri 27 Jan 2023 15:19 CET

Illustration photo: AFP

The French government has extended the renovating initiative MaPrimeRenov’ to make it available to all home owners, including for second homes, for grants worth potentially thousands of euros. Here's how to go about applying for the scheme.

Advertisement

What is it?

Launched back in January 2020, the government scheme MaPrimeRenov’ lets homeowners apply for financial help to renovate their homes.

Each household can test the renovation they would like to do using THIS simulator (more on this below). Typically, for households in the lowest income bracket, the maximum aid offered is €10,000, but this is set to increase in 2024. Keep in mind that the amount will depend on several factors, including the type of project, the household income and the number of people living there.

Advertisement

Previously reserved for modest-income households, the scheme has been expanded and is now available to everyone, including some high-income owners, landlords renting out their property and second-home owners.

Applicants do however need a French numéro fiscal (tax number) and a copy of their latest tax declaration, which means those who do not file the annual tax declaration in France are effectively excluded.

How is it set to change?

In 2023, the French government increased funding for the MaPrimeRenov by approximately €100 million. For households with the lowest incomes (meaning those who benefit from MaPrimeRenov "Sérénité"), the budget was raised by 21 percent.

This year, in 2024, the French government has announced plans to increase funding for the scheme by €1.6 billion. There will be some changes to accompany this rise in funding, primarily regarding the approach to homes with low energy ratings.

In France, properties considered to be the least efficient fall into the F and G categories. They are also known as passoires energetiques – energy sinks.

Starting in January, all properties applying for the scheme will need to submit their energy rating. For those properties categorised as F and G, they will need to aim to increase their energy rating (DPE) by at least two levels to be eligible for grants.

The second change coming in 2024 will be an increase in the maximum cap on the amount awarded to the lowest earning households for large-scale renovation work.

This will go up to €70,000, from €35,000 previously. Low-income households will also be able to benefit from zero-interest loans to cover any remaining expenses.

Large-scale renovation projects will also be managed in part by the independent third party group the 'National Housing Agency' (Agence nationale de l’habitat, Anah).

What kind of work is covered by the scheme?

The grant scheme covers four main categories of renovating work:

Heating (so changing the heater, for example, or installing a new system)

Insulation

Ventilation

Energy audits

However the company hired to renovate must be on the government-approved list of companies that qualify for the grant, which means they need the label RGE (Reconnue Garant de l’Environnement).

Who can access the grant scheme?

Only property owners can access the scheme, so not those renting.

The building needs to have been built at least 15 years ago. However, homes that are at least two years old can apply for the scheme if the objective is to finance the replacement of an oil-burning boiler with new heating or hot water supply equipment.

For several months only lower-income owners could benefit from the scheme, but in 2021 it became open to everyone.

At first the scheme was closed to second home owners, but a government decree published in January 2021 confirmed that it had been widened to include anyone "with a legal right to the property".

That includes co-owners, second-home owners and landlords who rent out their property.

Advertisement

Why is the government doing this?

MaPrimeRenov was part of the French government's relaunch plan after the pandemic. Its original goal was to stimulate the economy while transforming households into more environmentally friendly, less energy-hungry entities.

Now, the goal is to accelerate the clean-energy transition in France. The French government has the goal of 200,000 energy-related renovations in 2024, compared with 90,000 as of mid-2023.

Simulating your grant

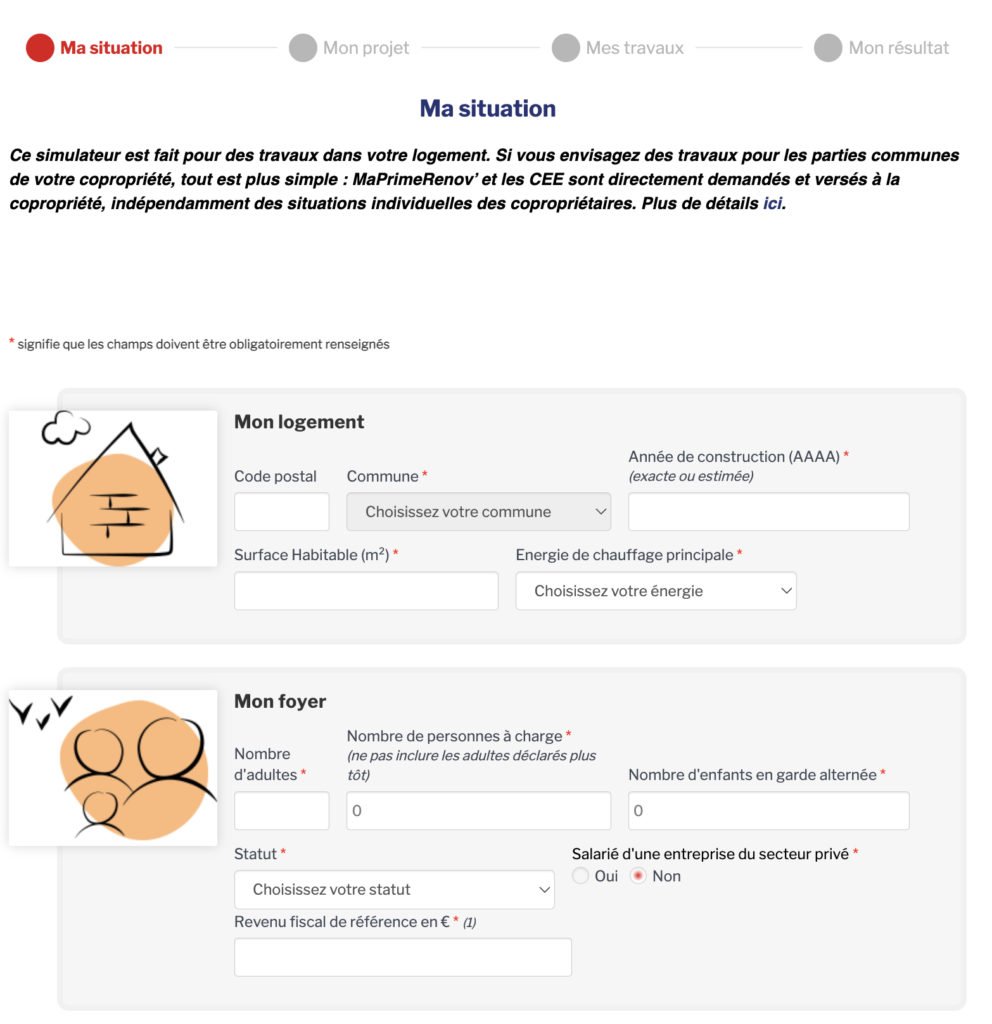

To simulate how large of a grant you might be eligible for you should first go to the website "https://france-renov.gouv.fr/aides/simulation". The home screen will ask you to choose the type of property you wish to apply the renovation aid to - either an apartment, a home, or a condominium.

Ma Prime Renov simulator (Credit: French government)

The next page will involve describing details about your home and where you live (postal code, size in metres squared, construction year, primary heating method). Then, you will provide information about your household (ex. number of dependents) and your reference tax income, which can be found on the first page of your last income tax notice.

Advertisement

Ma Prim Renov simulator (Credit: French government)

Ma Prim Renov simulator (Credit: French government)

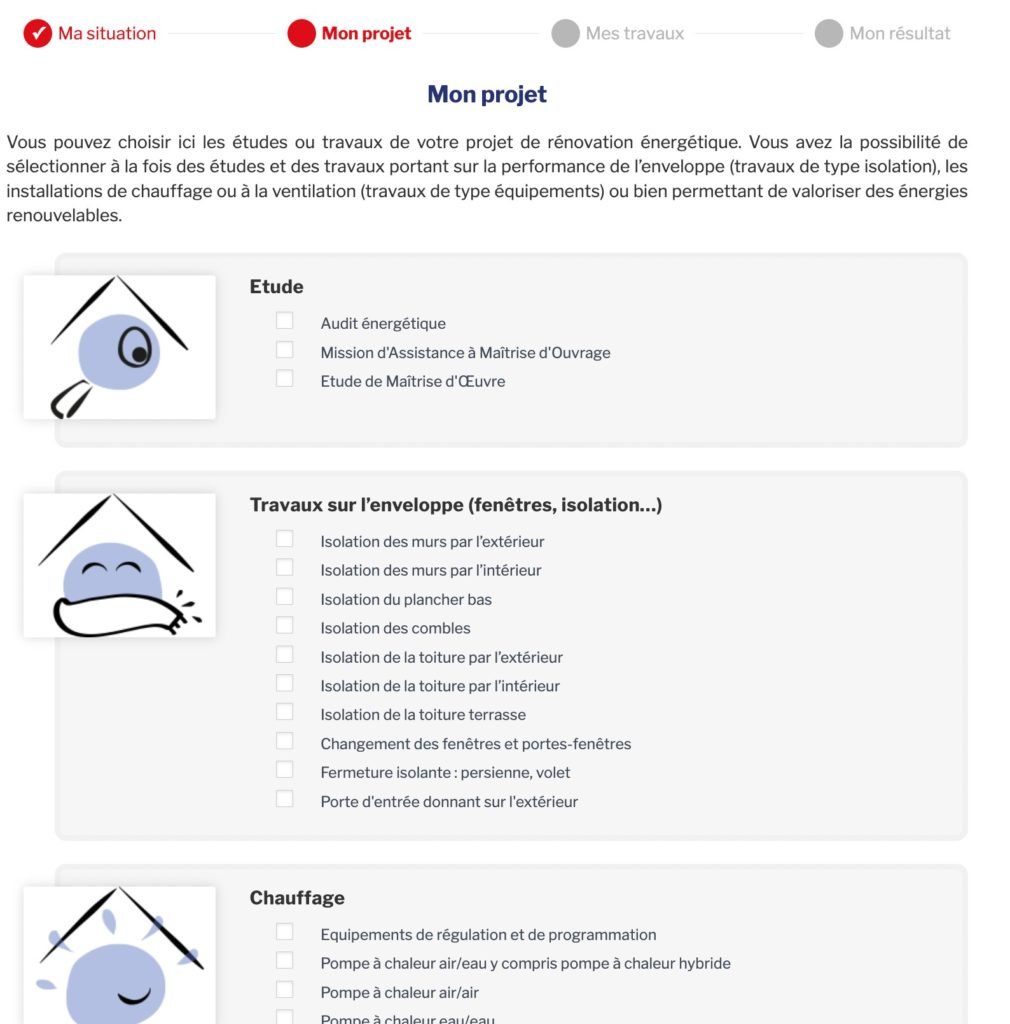

The next page will ask you to click on the relevant renovation work you would like to do. Keep in mind you can click on both an audit, as well as physical renovation work.

Ma Prim Renov simulator (Credit: French government)

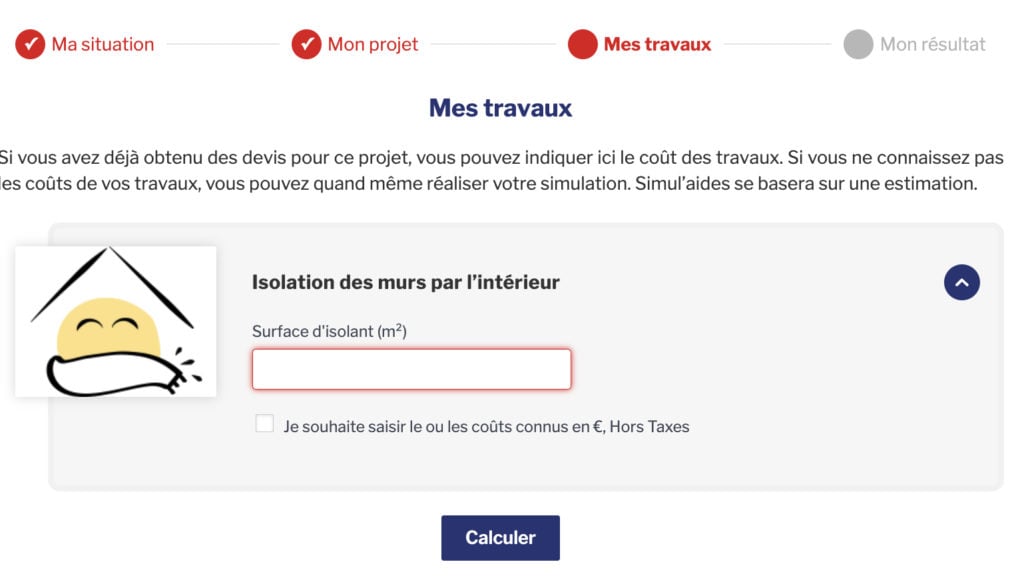

After choosing the renovation work that applies to you, then may have to give specific details - for instance, if you were looking to have your interior walls insulated, then you would need to provide the surface area squared in metres. At this point, you can also enter any known costs in euros, excluding taxes, to make the simulation more accurate.

Advertisement

The final page will offer you a simulated amount for the renovation project you would like to do. If your amount is zero, that means you may not qualify for this aid. However, if you believe you ought to qualify or if you have any questions, you can contact your local advisory office for MaPrimeRenov by entering your city or postal code at this LINK.

You can also take a look at your income threshold to get a better idea of whether you might qualify, and if so for how much.

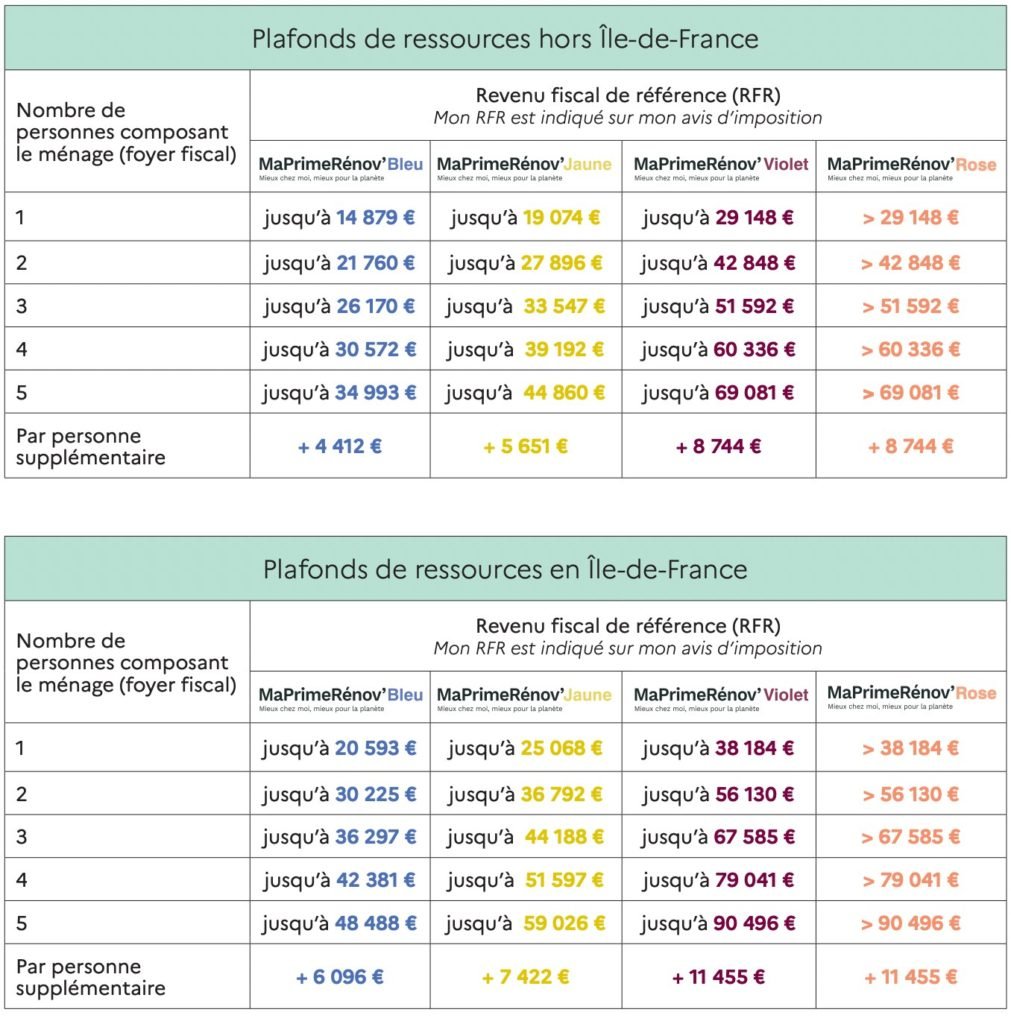

Income thresholds

To determine whether or not a project is eligible for the grant scheme and how much money the household gets, the government checks the total income of the household against the cost of the renovating project.

The income thresholds for households depend on the kind of services needed, outlined in four different MaPrimeRénov' schemes: blue, yellow, violet or pink (full list HERE).

While MaPrimeRénovBleu (blue) is typically restricted to modest-income households, the maximum income thresholds also depend on the number of people living in the property and whether or not it is located in greater Paris Île-de-France region.

Below you can see the income thresholds, as of 2021, for households outside the Paris region (on the top) and inside the Paris region (on the bottom).

Photo: French government

How do I apply?

To apply for a grant, you must create an account on maprimerenov.gouv.fr and connect to that account. In order to do this you will need a numéro fiscal, the number you use forfilling out your tax returns, plus other documents you use when filing your taxes (bank details - both French and international banks work - copy of your ID, etc).

Advertisement

You will be asked to provide:

A copy of your latest tax return

An email address and a phone number

Names and dates of birth of all members of the household

A dévis (builders' invoice) for the work done

The amount of any other help schemes or grants the household benefits from

Co-owner households must provide an attestation signed by all parties as well as information regarding the number of households in the home.

Only work done after October 1st, 2020 is accepted (so applicants need a dévis signed after that date).

A detailed guide to each step of the process can be found at maprimerenov.gouv.fr under the section "Me renseigner".

For more information and to access the grant, go to MaPrimeRénov'. You can also call +33 (0) 8 08 800 700 if you have specific questions on the scheme. You can also contact the office dedicated to serving your area - here is the link to find one near you.

If you want to search for a government approved renovating company in your area, go to this website, tap in your post code and type of work you want done and hit search.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

The link above takes you to a log in page - and not a registration page

It appears you need to register here https://www.maprimerenov.gouv.fr/prweb/PRAuth/BPNVwCpLW8TKW49zoQZpAw%5B%5B*/!@ebedc88a07b432bb739887648f6a418f!STANDARD

but the links dont seem to work - so registration is currently impossible

interested to know if anyone else has tried it

Photo: French government

Photo: French government

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.