Carte vitale: What your French health insurance card entitles you to

Everyone living legally in France is entitled to basic health insurance with their carte vitale. But it can be hard to get to grips with exactly which medical services you are reimbursed for and how much you get back. Here's a look at what you need to know.

The French health service - despite having problems - is known around the world for providing high quality healthcare at low prices.

However how low the cost really is varies greatly from person to person, with your age, financial situation, and whether or not you have top-up insurance known as a mutuelle - and how generous that is - all playing a part in how much you pay for your healthcare in France.

We've taking a look at what you can claim back from the French state with your carte vitale if you have the basic cover afforded by the card, with no top-up insurance.

READ ALSO: Assurance maladie: 5 things to know about France's public healthcare system

There are basically two areas to charging in French healthcare - appointments with medical professionals and then the cost of any treatment (medication, tests, scans or surgery) that they prescribe.

When you visit any kind of medical professional in France you will pay on the spot for the cost of the appointment, which can come as a surprise to Brits reared on the NHS's free at the point of delivery model.

However the medic will then swipe your carte vitale and the French state will reimburse you with some of the cost of the appointment.

What percentage of the cost you are reimbursed, however, is complicated and varies by many factors including your situation (your age, whether you are in work or studying) and by the type of doctor that you see.

Most people in France also have 'top-up' private insurance known as a mutuelle which takes care of the remaining percentage that the state doesn't reimburse (depending on the policy - not all mutuelles have full dental cover, for example).

Appointments

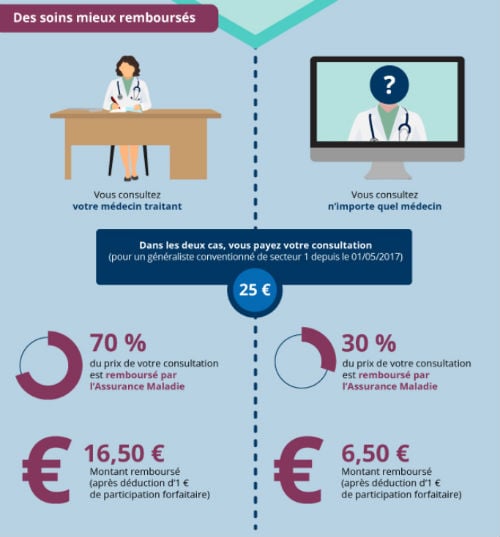

The standard charge for an appointment with a médecin généraliste (general practitioner or family doctors) is €25 and the standard reimbursement rate is 70 percent, so you pay €25 and the government pays you back €16.50. This amount is set to rise at the end of 2023 by €1.50 per appointment, meaning GP consultations will go up to €26.50

However, as with French grammar, there are lots of exceptions.

Doctors work under two sectors - sector one doctors mostly charge the standard €25 apart from in exceptional circumstances, while sector two doctors are entitled to charge more, and you will not get refunds for any amount over the €25 minimum.

You can check which sector a doctor works under on the official site of France's state health insurance ameli.fr and it will also be listed if you are booking an appointment through the Doctolib app.

But to get the full amount you are entitled to back, it is vitally important to choose a doctor as your main GP (médecin traitant) and use them as your first port of call for an appointment.

If you do not have a main GP registered on your card and visit them first so that they can refer you to any specialists, or you decide to visit a different GP, you will only receive 30 percent of the cost of your appointment back.

However sometimes the surgery where you GP works will assign you a different doctor for your appointment and in that case you will get the 70 percent reimbursement.

You will receive a form to declare your GP as part of your Carte Vitale pack when you apply for your card and you can also download the form here and send it off to your local CPAM (public health insurance body).

Women who are more than six months pregnant, may be able to claim 100 percent of the cost back, and to check out some of the other exceptions click here.

Diagram: Ameli.fr

Diagram: Ameli.fr

Appointments with specialists

Unlike in the UK, you can make appointments directly with a specialist without getting a referral from your GP first. But you will only get the standard 70 percent rate of reimbursement if you first visit the GP.

There are, of course, some exceptions to that rule.

You can have an appointment with gynecologists for periodic examinations, including screening, prescribing and monitoring contraception, monitoring pregnancy and abortions.

You can also visit ophthalmologists for certain kinds of appointments, and psychiatrists if you are aged 16-25- years-old.

For the full list, check out the ameli website.

Under 16s

If you have children aged under 16 then the cost of a visit to the doctor varies and, huge surprise, it can get a bit complicated.

If you have a child aged under 6, a visit to the GP listed as sector one will cost more than it does for an adult.

The standard health insurance approved price is €30 and this cost is refunded 70 percent as it is for adults, meaning you will be reimbursed €21.

Once your child turns 7 a trip to the doctor will cost €25.

However you may choose to take your child to a pediatrician, in which case an appointment will cost slightly more.

A trip to a pediatrician under sector one will cost €32 and is also subject to the 70 percent reimbursement rate, which means you'll get €22.40 back.

If your child is aged 7-16 and you choose to visit a pediatrician, the standard price for an appointment is €28.

For more information on this, visit ameli.fr.

Treatments

Once the appointment is done the medic is likely to decide upon a course of treatment or prescribe some medication.

With prescriptions, you pay the pharmacist for the cost of the drugs, and then you are reimbursed some of the cost.

The general rule for medication is that 100 per cent of the cost is reimbursed if the drug is "irreplaceable", such as drugs to treeat diabetes, AIDS, cancer and other chronic diseases.

If the medication is determined to be "a major or important medical service", such as antibiotics, then you get 65 percent back.

Drugs that have only "moderate" medical benefits and homeopathic remedies are reimbursed at 30 per cent.

While drugs that have only "low" medical value are reimbursed at 15 percent.

The thing to watch out for is generic drugs. Generally your GP will prescribe the generic drug, and if not the pharmacist will point out that there is a generic available if you want. You are free to refuse the generic and opt for a brand-name drug if you prefer, but the reimbursement will only cover the cost of the cheaper generic drug.

Ameli advises: "Do not hesitate to ask your doctor to prescribe a generic drug for you, and to accept a generic drug when your pharmacist offers it to you. You will be just as well cared for and spend less."

Comments (1)

See Also

The French health service - despite having problems - is known around the world for providing high quality healthcare at low prices.

However how low the cost really is varies greatly from person to person, with your age, financial situation, and whether or not you have top-up insurance known as a mutuelle - and how generous that is - all playing a part in how much you pay for your healthcare in France.

We've taking a look at what you can claim back from the French state with your carte vitale if you have the basic cover afforded by the card, with no top-up insurance.

READ ALSO: Assurance maladie: 5 things to know about France's public healthcare system

There are basically two areas to charging in French healthcare - appointments with medical professionals and then the cost of any treatment (medication, tests, scans or surgery) that they prescribe.

When you visit any kind of medical professional in France you will pay on the spot for the cost of the appointment, which can come as a surprise to Brits reared on the NHS's free at the point of delivery model.

However the medic will then swipe your carte vitale and the French state will reimburse you with some of the cost of the appointment.

What percentage of the cost you are reimbursed, however, is complicated and varies by many factors including your situation (your age, whether you are in work or studying) and by the type of doctor that you see.

Most people in France also have 'top-up' private insurance known as a mutuelle which takes care of the remaining percentage that the state doesn't reimburse (depending on the policy - not all mutuelles have full dental cover, for example).

Appointments

The standard charge for an appointment with a médecin généraliste (general practitioner or family doctors) is €25 and the standard reimbursement rate is 70 percent, so you pay €25 and the government pays you back €16.50. This amount is set to rise at the end of 2023 by €1.50 per appointment, meaning GP consultations will go up to €26.50

However, as with French grammar, there are lots of exceptions.

Doctors work under two sectors - sector one doctors mostly charge the standard €25 apart from in exceptional circumstances, while sector two doctors are entitled to charge more, and you will not get refunds for any amount over the €25 minimum.

You can check which sector a doctor works under on the official site of France's state health insurance ameli.fr and it will also be listed if you are booking an appointment through the Doctolib app.

But to get the full amount you are entitled to back, it is vitally important to choose a doctor as your main GP (médecin traitant) and use them as your first port of call for an appointment.

If you do not have a main GP registered on your card and visit them first so that they can refer you to any specialists, or you decide to visit a different GP, you will only receive 30 percent of the cost of your appointment back.

However sometimes the surgery where you GP works will assign you a different doctor for your appointment and in that case you will get the 70 percent reimbursement.

You will receive a form to declare your GP as part of your Carte Vitale pack when you apply for your card and you can also download the form here and send it off to your local CPAM (public health insurance body).

Women who are more than six months pregnant, may be able to claim 100 percent of the cost back, and to check out some of the other exceptions click here.

Appointments with specialists

Unlike in the UK, you can make appointments directly with a specialist without getting a referral from your GP first. But you will only get the standard 70 percent rate of reimbursement if you first visit the GP.

There are, of course, some exceptions to that rule.

You can have an appointment with gynecologists for periodic examinations, including screening, prescribing and monitoring contraception, monitoring pregnancy and abortions.

You can also visit ophthalmologists for certain kinds of appointments, and psychiatrists if you are aged 16-25- years-old.

For the full list, check out the ameli website.

Under 16s

If you have children aged under 16 then the cost of a visit to the doctor varies and, huge surprise, it can get a bit complicated.

If you have a child aged under 6, a visit to the GP listed as sector one will cost more than it does for an adult.

The standard health insurance approved price is €30 and this cost is refunded 70 percent as it is for adults, meaning you will be reimbursed €21.

Once your child turns 7 a trip to the doctor will cost €25.

However you may choose to take your child to a pediatrician, in which case an appointment will cost slightly more.

A trip to a pediatrician under sector one will cost €32 and is also subject to the 70 percent reimbursement rate, which means you'll get €22.40 back.

If your child is aged 7-16 and you choose to visit a pediatrician, the standard price for an appointment is €28.

For more information on this, visit ameli.fr.

Treatments

Once the appointment is done the medic is likely to decide upon a course of treatment or prescribe some medication.

With prescriptions, you pay the pharmacist for the cost of the drugs, and then you are reimbursed some of the cost.

The general rule for medication is that 100 per cent of the cost is reimbursed if the drug is "irreplaceable", such as drugs to treeat diabetes, AIDS, cancer and other chronic diseases.

If the medication is determined to be "a major or important medical service", such as antibiotics, then you get 65 percent back.

Drugs that have only "moderate" medical benefits and homeopathic remedies are reimbursed at 30 per cent.

While drugs that have only "low" medical value are reimbursed at 15 percent.

The thing to watch out for is generic drugs. Generally your GP will prescribe the generic drug, and if not the pharmacist will point out that there is a generic available if you want. You are free to refuse the generic and opt for a brand-name drug if you prefer, but the reimbursement will only cover the cost of the cheaper generic drug.

Ameli advises: "Do not hesitate to ask your doctor to prescribe a generic drug for you, and to accept a generic drug when your pharmacist offers it to you. You will be just as well cared for and spend less."

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.