Property

For Members

Renting in Paris: Ten things you need to know about apartment hunting

The Local France - [email protected]

Published: 25 Jul, 2018 CET.

Updated: Wed 25 Jul 2018 09:42 CET

Let's face it, finding a flat to rent in Paris can be a nightmare. Real estate agency Lodgis shares ten things you really need to know about apartment hunting in the French capital.

1. Get a three-month headstart (at least)

Competition is fierce when it comes to renting an apartment in Paris, so get planning early.

For the short-term stays we recommend that you book your apartment at least three months before, or six months for the long-term stays.

If you do it too late, you might miss an opportunity - not to mention that some owners might think that you're going to change your mind seeing as you'd be operating at the last minute.

Photo: AFP

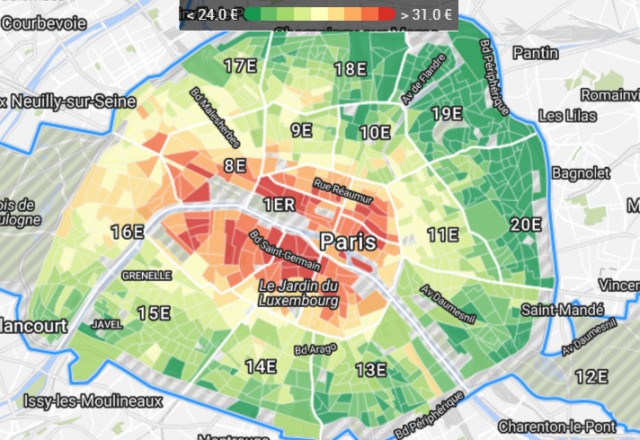

2. Learn the prices per square metre across Paris

The price for your surface area changes in different parts of the city, and this is good to know when you're figuring out your budget.

The price per sqm is highest in the 1st arrondissement of Paris (at €30.70 per sqm), for example, while it's lowest in the 19th arrondissement at €22.80.

Most people think that they need to break the bank to live in a big Paris apartment, but this is totally wrong if you're prepared to live in a cheaper area.

Here is a good place to start if you're looking for the average rental prices per sqm (or get a rough idea from the map below).

Photo: AFP

2. Learn the prices per square metre across Paris

The price for your surface area changes in different parts of the city, and this is good to know when you're figuring out your budget.

The price per sqm is highest in the 1st arrondissement of Paris (at €30.70 per sqm), for example, while it's lowest in the 19th arrondissement at €22.80.

Most people think that they need to break the bank to live in a big Paris apartment, but this is totally wrong if you're prepared to live in a cheaper area.

Here is a good place to start if you're looking for the average rental prices per sqm (or get a rough idea from the map below).

3. Don't forget the charges

Some affordable-sounding flats in Paris come with very high charges, so never neglect that part.

Ask about if there are charges for things like the water, the elevator, the cleaning services of the building, or even the garden maintenance.

3. Don't forget the charges

Some affordable-sounding flats in Paris come with very high charges, so never neglect that part.

Ask about if there are charges for things like the water, the elevator, the cleaning services of the building, or even the garden maintenance.

Photo: Ana Paula Hirama/WikiCommons

4. Have you considered transport?

Public transport in Paris is way cheaper than having a car (but if you do drive, skip ahead to the next point).

With this in mind, you're going to be taking public transport - so find out if your potential home has good connections.

Download the RATP app and plug in the address, find out how well it connects to your office (and indeed anywhere else that you go).

And it's not just buses and Metro stations, check in with the Velib' bike stops.

The Velib' bike rental service is going through a period of upheaval at the moment but the City is hopeful of getting it back up and running soon.

In the meantime, if your preferred way of travelling around Paris is cycling, make sure you check whether there is somewhere to store your bike in a potential apartment or whether there is somewhere to leave your bike securely on the street.

Photo: Ana Paula Hirama/WikiCommons

4. Have you considered transport?

Public transport in Paris is way cheaper than having a car (but if you do drive, skip ahead to the next point).

With this in mind, you're going to be taking public transport - so find out if your potential home has good connections.

Download the RATP app and plug in the address, find out how well it connects to your office (and indeed anywhere else that you go).

And it's not just buses and Metro stations, check in with the Velib' bike stops.

The Velib' bike rental service is going through a period of upheaval at the moment but the City is hopeful of getting it back up and running soon.

In the meantime, if your preferred way of travelling around Paris is cycling, make sure you check whether there is somewhere to store your bike in a potential apartment or whether there is somewhere to leave your bike securely on the street.

Photo: AFP

5. Does it come with a car park?

For those who have a car, make sure that you ask if the apartment you want to rent includes a parking spot. This is a fact that surprises a lot of foreigners but, in Paris, most apartments don't offer parking, in which case you have to rent a parking spot near your apartment (which can prove to be costly indeed).

Photo: AFP

5. Does it come with a car park?

For those who have a car, make sure that you ask if the apartment you want to rent includes a parking spot. This is a fact that surprises a lot of foreigners but, in Paris, most apartments don't offer parking, in which case you have to rent a parking spot near your apartment (which can prove to be costly indeed).

Photo: Benh LIEU SONG/WikiCommons

6. Be prepared with your "dossier"

This is a crucial tip. Everyone knows France is famous for loving paperwork and administrative procedures, and renting a home is no exception.

It's all about security, and in this case the paperwork is to reassure the owner that they're not renting their apartment to a total stranger.

The documents won't be the same for a long-term and a short-term rental, but here is a guide.

The documents you will likely need are:

Everyone

- Passport

- Insurance certificate

- Your bank details

Long-term professional:

- Your last three payslips and your employment contract

- Mission order

Long-term student:

- Education enrollment certificate

- Guarantors' three last payslips or employee certification

7. Do you need a guarantor?

If you're a student you will most likely need to prove that you can afford the apartment, and this means getting a guarantor - or essentially someone who will promise to stump up the money if you can't.

Some owners accept international guarantors, but others don't - and you'll have to tackle this on a case by case basis.

Obviously if you already have a job in Paris with the three payslips and the work contract then you don't need a guarantor.

Photo: Benh LIEU SONG/WikiCommons

6. Be prepared with your "dossier"

This is a crucial tip. Everyone knows France is famous for loving paperwork and administrative procedures, and renting a home is no exception.

It's all about security, and in this case the paperwork is to reassure the owner that they're not renting their apartment to a total stranger.

The documents won't be the same for a long-term and a short-term rental, but here is a guide.

The documents you will likely need are:

Everyone

- Passport

- Insurance certificate

- Your bank details

Long-term professional:

- Your last three payslips and your employment contract

- Mission order

Long-term student:

- Education enrollment certificate

- Guarantors' three last payslips or employee certification

7. Do you need a guarantor?

If you're a student you will most likely need to prove that you can afford the apartment, and this means getting a guarantor - or essentially someone who will promise to stump up the money if you can't.

Some owners accept international guarantors, but others don't - and you'll have to tackle this on a case by case basis.

Obviously if you already have a job in Paris with the three payslips and the work contract then you don't need a guarantor.

Photo: Max Pixel

8. Be prepared for the deposit(s)

There are two types of these - the apartment deposit (acompte) and the security deposit.

The first, the acompte, is paid by the tenant after signing the lease in order to officially book the apartment. It should be paid with the first rental payment.

- No acompte is needed for rentals of under three weeks

- You need 30 percent of your rent if you're staying between three weeks and three months

- One month of rent if you're staying longer than three months

The security deposit is not always necessary and depends on the owner. The amount is calculated according to the duration of your stay:

- From 21 to 60 days: 50 perent of one month's rent

- From 2 to 6 months: 1 month rent

- More than 6 months: 2 months rent.

You will get your security deposit back 10 days after your departure.

However, if there are damages identified in the apartment, the repairing costs will be deducted from the security deposit and you will get the remaining amount 60 days after your departure. This is why we recommend that you read your contract very carefully and don't hesitate to ask questions to the owner or the agency in charge of your dossier.

9. Do I need to pay the council tax?

The Council Tax (in French "taxe d'habitation"), is a local property tax implemented by the area in which your property is located. It can be paid by the owner or by the tenant depending on certain conditions.

If you are occupying the apartment on January 1st as “main residence” for more than 8 consecutive months, the tenant will have to pay the council-tax whether he is a professional or a student.

The amount of the council tax depends on the arrondissement you live in, your financial profile, the rent you pay and the property management costs.

Photo: Max Pixel

8. Be prepared for the deposit(s)

There are two types of these - the apartment deposit (acompte) and the security deposit.

The first, the acompte, is paid by the tenant after signing the lease in order to officially book the apartment. It should be paid with the first rental payment.

- No acompte is needed for rentals of under three weeks

- You need 30 percent of your rent if you're staying between three weeks and three months

- One month of rent if you're staying longer than three months

The security deposit is not always necessary and depends on the owner. The amount is calculated according to the duration of your stay:

- From 21 to 60 days: 50 perent of one month's rent

- From 2 to 6 months: 1 month rent

- More than 6 months: 2 months rent.

You will get your security deposit back 10 days after your departure.

However, if there are damages identified in the apartment, the repairing costs will be deducted from the security deposit and you will get the remaining amount 60 days after your departure. This is why we recommend that you read your contract very carefully and don't hesitate to ask questions to the owner or the agency in charge of your dossier.

9. Do I need to pay the council tax?

The Council Tax (in French "taxe d'habitation"), is a local property tax implemented by the area in which your property is located. It can be paid by the owner or by the tenant depending on certain conditions.

If you are occupying the apartment on January 1st as “main residence” for more than 8 consecutive months, the tenant will have to pay the council-tax whether he is a professional or a student.

The amount of the council tax depends on the arrondissement you live in, your financial profile, the rent you pay and the property management costs.

Photo: Max Pixel

10. Do I need an insurance?

No matter what type of apartment you are leasing, whether it's short or long-term you will need to take out an insurance policy in order to cover potential risks (water damage, fire, robbery).

The subscription to the insurance is very simple and can be done on the internet for example on the French Furnished Insurance website.

It's called an "assurance d'habitation" in French and it can be provided by the bank or even from your country. But remember, if there is a problem the French law has the priority, which is the reason why we always recommend the insurance to be french.

This article was put together by the team at Lodgis, which advertises properties to rent and for sale across Paris.

Find their English site here and their blog here, which contains loads of useful information about living in Paris.

Photo: Max Pixel

10. Do I need an insurance?

No matter what type of apartment you are leasing, whether it's short or long-term you will need to take out an insurance policy in order to cover potential risks (water damage, fire, robbery).

The subscription to the insurance is very simple and can be done on the internet for example on the French Furnished Insurance website.

It's called an "assurance d'habitation" in French and it can be provided by the bank or even from your country. But remember, if there is a problem the French law has the priority, which is the reason why we always recommend the insurance to be french.

This article was put together by the team at Lodgis, which advertises properties to rent and for sale across Paris.

Find their English site here and their blog here, which contains loads of useful information about living in Paris.

Comments

See Also

1. Get a three-month headstart (at least)

Competition is fierce when it comes to renting an apartment in Paris, so get planning early.

For the short-term stays we recommend that you book your apartment at least three months before, or six months for the long-term stays.

If you do it too late, you might miss an opportunity - not to mention that some owners might think that you're going to change your mind seeing as you'd be operating at the last minute.

Photo: AFP

2. Learn the prices per square metre across Paris

The price for your surface area changes in different parts of the city, and this is good to know when you're figuring out your budget.

The price per sqm is highest in the 1st arrondissement of Paris (at €30.70 per sqm), for example, while it's lowest in the 19th arrondissement at €22.80.

Most people think that they need to break the bank to live in a big Paris apartment, but this is totally wrong if you're prepared to live in a cheaper area.

Here is a good place to start if you're looking for the average rental prices per sqm (or get a rough idea from the map below).

3. Don't forget the charges

Some affordable-sounding flats in Paris come with very high charges, so never neglect that part.

Ask about if there are charges for things like the water, the elevator, the cleaning services of the building, or even the garden maintenance.

Photo: Ana Paula Hirama/WikiCommons

4. Have you considered transport?

Public transport in Paris is way cheaper than having a car (but if you do drive, skip ahead to the next point).

With this in mind, you're going to be taking public transport - so find out if your potential home has good connections.

Download the RATP app and plug in the address, find out how well it connects to your office (and indeed anywhere else that you go).

And it's not just buses and Metro stations, check in with the Velib' bike stops.

The Velib' bike rental service is going through a period of upheaval at the moment but the City is hopeful of getting it back up and running soon.

In the meantime, if your preferred way of travelling around Paris is cycling, make sure you check whether there is somewhere to store your bike in a potential apartment or whether there is somewhere to leave your bike securely on the street.

Photo: AFP

5. Does it come with a car park?

For those who have a car, make sure that you ask if the apartment you want to rent includes a parking spot. This is a fact that surprises a lot of foreigners but, in Paris, most apartments don't offer parking, in which case you have to rent a parking spot near your apartment (which can prove to be costly indeed).

Photo: Benh LIEU SONG/WikiCommons

6. Be prepared with your "dossier"

This is a crucial tip. Everyone knows France is famous for loving paperwork and administrative procedures, and renting a home is no exception.

It's all about security, and in this case the paperwork is to reassure the owner that they're not renting their apartment to a total stranger.

The documents won't be the same for a long-term and a short-term rental, but here is a guide.

The documents you will likely need are:

Everyone

- Passport

- Insurance certificate

- Your bank details

Long-term professional:

- Your last three payslips and your employment contract

- Mission order

Long-term student:

- Education enrollment certificate

- Guarantors' three last payslips or employee certification

7. Do you need a guarantor?

If you're a student you will most likely need to prove that you can afford the apartment, and this means getting a guarantor - or essentially someone who will promise to stump up the money if you can't.

Some owners accept international guarantors, but others don't - and you'll have to tackle this on a case by case basis.

Obviously if you already have a job in Paris with the three payslips and the work contract then you don't need a guarantor.

Photo: Max Pixel

8. Be prepared for the deposit(s)

There are two types of these - the apartment deposit (acompte) and the security deposit.

The first, the acompte, is paid by the tenant after signing the lease in order to officially book the apartment. It should be paid with the first rental payment.

- No acompte is needed for rentals of under three weeks

- You need 30 percent of your rent if you're staying between three weeks and three months

- One month of rent if you're staying longer than three months

The security deposit is not always necessary and depends on the owner. The amount is calculated according to the duration of your stay:

- From 21 to 60 days: 50 perent of one month's rent

- From 2 to 6 months: 1 month rent

- More than 6 months: 2 months rent.

You will get your security deposit back 10 days after your departure.

However, if there are damages identified in the apartment, the repairing costs will be deducted from the security deposit and you will get the remaining amount 60 days after your departure. This is why we recommend that you read your contract very carefully and don't hesitate to ask questions to the owner or the agency in charge of your dossier.

9. Do I need to pay the council tax?

The Council Tax (in French "taxe d'habitation"), is a local property tax implemented by the area in which your property is located. It can be paid by the owner or by the tenant depending on certain conditions.

If you are occupying the apartment on January 1st as “main residence” for more than 8 consecutive months, the tenant will have to pay the council-tax whether he is a professional or a student.

The amount of the council tax depends on the arrondissement you live in, your financial profile, the rent you pay and the property management costs.

Photo: Max Pixel

10. Do I need an insurance?

No matter what type of apartment you are leasing, whether it's short or long-term you will need to take out an insurance policy in order to cover potential risks (water damage, fire, robbery).

The subscription to the insurance is very simple and can be done on the internet for example on the French Furnished Insurance website.

It's called an "assurance d'habitation" in French and it can be provided by the bank or even from your country. But remember, if there is a problem the French law has the priority, which is the reason why we always recommend the insurance to be french.

This article was put together by the team at Lodgis, which advertises properties to rent and for sale across Paris.

Find their English site here and their blog here, which contains loads of useful information about living in Paris.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.