How the Brexit vote affects your British pension in France

The Local France - [email protected]

Published: 20 Jul, 2016 CET.

Updated: Wed 20 Jul 2016 11:03 CET

Des Cooney from Axis Strategy Consultants looks at how the UK state pension will be affected by Brexit and what expats in France can do to protect their money.

The decision by UK voters to leave the European Union has been unsettling for expats based in Europe. As their status becomes uncertain there is increased concern felt by many British, especially on the pension front. The Brexit vote will have a major impact on the UK economy in the months and years ahead and could have far-reaching consequences for pensioners living abroad.

The political landscape is continuously shifting with financial markets reacting to every move. For British expats in France, who are dependent on income from the UK, the recent decline in sterling of circa 10 percent may pose a significant challenge, as their purchasing power is linked to the value of the pound. As such, the proceeds of British pensions, inheritances or rental income will now buy less in France.

How will the UK state pension be affected?

Concerns that UK state pensions may be frozen have become real now that Britain has chosen to leave the EU. Under the existing system, the state pensions of retired Britons in Europe increase annually in line with either inflation or a figure of 2.5 percent; whichever is the highest.

The aim of this policy was to make it easier for people to move freely between EU countries during their working life without suffering penalties in retirement for doing so. The "no" vote has now created a predicament wherein existing bilateral agreements between the UK and countries in the European Economic Area (EEA) will have to be renegotiated. If no new agreement is reached, the UK’s DWP has confirmed that the state pension could be frozen i.e. no future annual increases.

At present the flat-rate state pension is set at £155.65 per week. Failure to secure a suitable arrangement would mean that the reported 472,000 EU-based British citizens aged 65 and over, who are currently in receipt of the state pension, would run the risk of losing up to £50,000 in pension increases over a 20-year period.

Government figures from 2015 show that there were around 61,000 British recipients of UK state pensions resident in France. The UK government has pledged to negotiate protections for expat pensioners in the wake of the Brexit vote. However, such negotiations are not straightforward; the process is likely to take a considerable amount of time.

Pressure on expats to return to the UK

Any changes to the existing system are likely to have a negative impact on pensioners who rely on their benefits keeping in line with inflation. There are fears since the Brexit vote that a large number of pensioners currently living in the EU may have no choice but to return to the UK. This particular problem would be exacerbated if Member State governments were to stop or restrict access to free healthcare. Retired British expats may suddenly find themselves having to pay for private medical cover in France, which would put an even greater strain on their financial resources.

What to do with private pensions

With a number of experts forecasting a possible recession in the UK, it is important for investors to review their pension funds to ensure that they are suitably diversified in terms of asset allocation. Warnings of a slump in the commercial and residential property market along with a cooling banking sector are signs of an economic downturn.

For those with Defined Benefit (DB) pension schemes, it is likely that falling gilt yields as a result of the ‘no’ vote will further drive up pension deficits. Brexit triggered a rush of investors to buy the safest government bonds, pushing prices up and yields down. As a consequence, the UK’s 6,000 private sector DB schemes, which guaranteed inflation-linked annual incomes based on salaries to 11 million workers, now find themselves struggling to meet their pension promises.

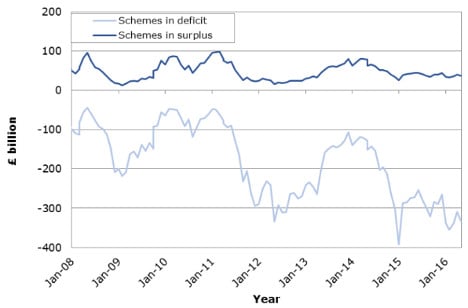

The latest figures suggest that 5,000 DB schemes are now in deficit; as such there is increasing pressure for the Pension Protection Fund (PPF), the government’s lifeboat fund, to come to pensioners rescue. Unfortunately, the shortfall between assets and liabilities in all UK schemes has actually risen from £820bn on the day of the EU referendum to £925bn as of the end of last week. The problem for the PPF is that it now runs the risk of being overwhelmed.

Based on 5945 schemes in the PPF 7800 index (Souce: PPF)

Take back control of your UK pension

One positive aspect of a reduction in gilt yields is the increase in transfer values wherein DB schemes increasingly look to offload liabilities by offering members attractive payouts as an alternative to a guaranteed income stream.

Although such a move will exert further pressure on the DB schemes themselves, it is indeed good news for those wishing to transfer out of such schemes. The downside is that any continuous deterioration in the funding levels of schemes may result in a liquidity crisis for the pension sponsor. A ‘run’ on transfers out of schemes may eventually result in a freeze on all transfers out by individuals.

In the mean-time expats should consider taking back control of their UK pensions whilst the window of opportunity exists. This can be done by transferring to a Qualifying Recognised Overseas Pension Scheme (QROPS). Under existing legislation expats can transfer to a QROPS and benefit from the choice of currency along with a much wider range of investment funds on offer from providers.

Whilst uncertainty remains in the British economy we can expect to experience ups and downs in the value of our pension savings. The challenge is to try and manage such movements by adopting a more nuanced approach to pension planning.

For more visit www.Axis-finance.com

Based on 5945 schemes in the PPF 7800 index (Souce: PPF)

Take back control of your UK pension

One positive aspect of a reduction in gilt yields is the increase in transfer values wherein DB schemes increasingly look to offload liabilities by offering members attractive payouts as an alternative to a guaranteed income stream.

Although such a move will exert further pressure on the DB schemes themselves, it is indeed good news for those wishing to transfer out of such schemes. The downside is that any continuous deterioration in the funding levels of schemes may result in a liquidity crisis for the pension sponsor. A ‘run’ on transfers out of schemes may eventually result in a freeze on all transfers out by individuals.

In the mean-time expats should consider taking back control of their UK pensions whilst the window of opportunity exists. This can be done by transferring to a Qualifying Recognised Overseas Pension Scheme (QROPS). Under existing legislation expats can transfer to a QROPS and benefit from the choice of currency along with a much wider range of investment funds on offer from providers.

Whilst uncertainty remains in the British economy we can expect to experience ups and downs in the value of our pension savings. The challenge is to try and manage such movements by adopting a more nuanced approach to pension planning.

For more visit www.Axis-finance.com

By Des Cooney, AXIS Strategy Consultants

By Des Cooney, AXIS Strategy Consultants

Comments

See Also

The decision by UK voters to leave the European Union has been unsettling for expats based in Europe. As their status becomes uncertain there is increased concern felt by many British, especially on the pension front. The Brexit vote will have a major impact on the UK economy in the months and years ahead and could have far-reaching consequences for pensioners living abroad.

The political landscape is continuously shifting with financial markets reacting to every move. For British expats in France, who are dependent on income from the UK, the recent decline in sterling of circa 10 percent may pose a significant challenge, as their purchasing power is linked to the value of the pound. As such, the proceeds of British pensions, inheritances or rental income will now buy less in France.

How will the UK state pension be affected?

Concerns that UK state pensions may be frozen have become real now that Britain has chosen to leave the EU. Under the existing system, the state pensions of retired Britons in Europe increase annually in line with either inflation or a figure of 2.5 percent; whichever is the highest.

The aim of this policy was to make it easier for people to move freely between EU countries during their working life without suffering penalties in retirement for doing so. The "no" vote has now created a predicament wherein existing bilateral agreements between the UK and countries in the European Economic Area (EEA) will have to be renegotiated. If no new agreement is reached, the UK’s DWP has confirmed that the state pension could be frozen i.e. no future annual increases.

At present the flat-rate state pension is set at £155.65 per week. Failure to secure a suitable arrangement would mean that the reported 472,000 EU-based British citizens aged 65 and over, who are currently in receipt of the state pension, would run the risk of losing up to £50,000 in pension increases over a 20-year period.

Government figures from 2015 show that there were around 61,000 British recipients of UK state pensions resident in France. The UK government has pledged to negotiate protections for expat pensioners in the wake of the Brexit vote. However, such negotiations are not straightforward; the process is likely to take a considerable amount of time.

Pressure on expats to return to the UK

Any changes to the existing system are likely to have a negative impact on pensioners who rely on their benefits keeping in line with inflation. There are fears since the Brexit vote that a large number of pensioners currently living in the EU may have no choice but to return to the UK. This particular problem would be exacerbated if Member State governments were to stop or restrict access to free healthcare. Retired British expats may suddenly find themselves having to pay for private medical cover in France, which would put an even greater strain on their financial resources.

What to do with private pensions

With a number of experts forecasting a possible recession in the UK, it is important for investors to review their pension funds to ensure that they are suitably diversified in terms of asset allocation. Warnings of a slump in the commercial and residential property market along with a cooling banking sector are signs of an economic downturn.

For those with Defined Benefit (DB) pension schemes, it is likely that falling gilt yields as a result of the ‘no’ vote will further drive up pension deficits. Brexit triggered a rush of investors to buy the safest government bonds, pushing prices up and yields down. As a consequence, the UK’s 6,000 private sector DB schemes, which guaranteed inflation-linked annual incomes based on salaries to 11 million workers, now find themselves struggling to meet their pension promises.

The latest figures suggest that 5,000 DB schemes are now in deficit; as such there is increasing pressure for the Pension Protection Fund (PPF), the government’s lifeboat fund, to come to pensioners rescue. Unfortunately, the shortfall between assets and liabilities in all UK schemes has actually risen from £820bn on the day of the EU referendum to £925bn as of the end of last week. The problem for the PPF is that it now runs the risk of being overwhelmed.

Based on 5945 schemes in the PPF 7800 index (Souce: PPF)

Take back control of your UK pension

One positive aspect of a reduction in gilt yields is the increase in transfer values wherein DB schemes increasingly look to offload liabilities by offering members attractive payouts as an alternative to a guaranteed income stream.

Although such a move will exert further pressure on the DB schemes themselves, it is indeed good news for those wishing to transfer out of such schemes. The downside is that any continuous deterioration in the funding levels of schemes may result in a liquidity crisis for the pension sponsor. A ‘run’ on transfers out of schemes may eventually result in a freeze on all transfers out by individuals.

In the mean-time expats should consider taking back control of their UK pensions whilst the window of opportunity exists. This can be done by transferring to a Qualifying Recognised Overseas Pension Scheme (QROPS). Under existing legislation expats can transfer to a QROPS and benefit from the choice of currency along with a much wider range of investment funds on offer from providers.

Whilst uncertainty remains in the British economy we can expect to experience ups and downs in the value of our pension savings. The challenge is to try and manage such movements by adopting a more nuanced approach to pension planning.

For more visit www.Axis-finance.com

By Des Cooney, AXIS Strategy Consultants

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.